Many people falsely believe that life insurance for diabetics doesn’t exist. In reality, there are quite a few life insurance options for the 34.2 million Americans who have diabetes.

While diabetes remains a health challenge for many, it is still very possible to secure good life insurance as a diabetic. Here are some key things to know about getting life insurance if you have diabetes.

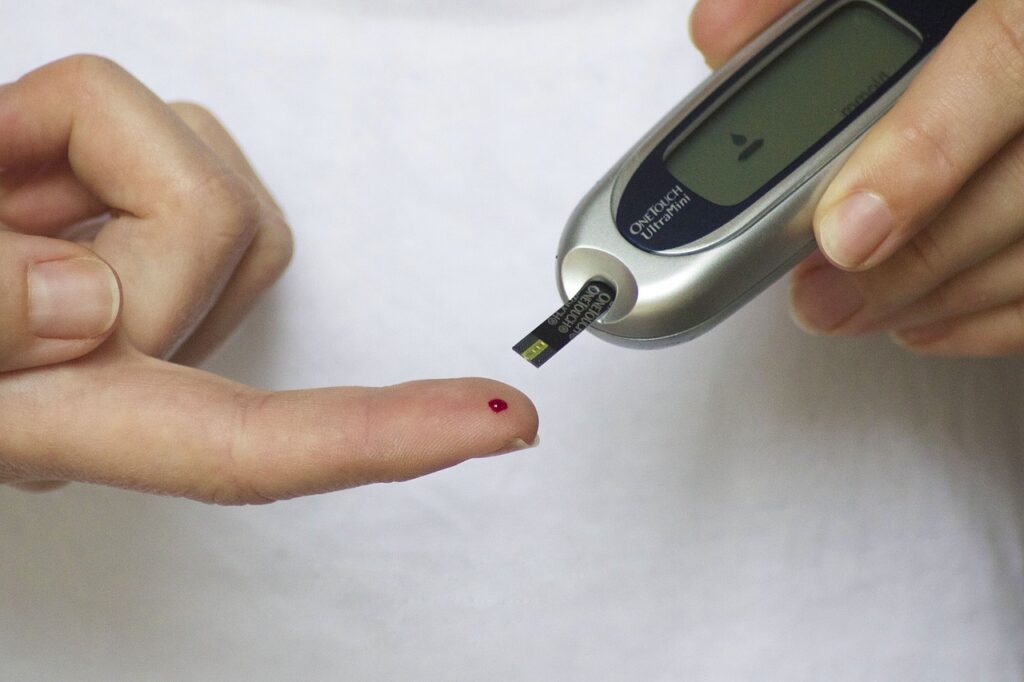

Insurance companies consider many factors.

In addition to knowing whether you have diabetes, a life insurer may also want to know:

- Whether you have Type 1 or Type 2 diabetes

- The age you were diagnosed with diabetes

- What medications you’re taking

- Your height and weight

- How well you’re controlling your diabetes

- Your glucose levels

- If you have other health conditions like heart disease and/or high blood pressure

- If you smoke

- Your overall medical history

- Your family history

Some life insurers offer something known as “clinical underwriting.” (Underwriting is when an insurance company evaluates you for coverage.) This type of underwriting takes a more holistic view of your health instead of zeroing in on certain risk factors. An insurance professional will know more about companies that offer clinical underwriting.

Life insurance for diabetics underwriting varies by insurer.

One person who knows a lot about life insurance for diabetics is Jake Irving. He’s is a licensed insurance agent and owner of Willamette Life Insurance in Beaverton, Oregon. Irving specializes in helping people with diabetes get life insurance. He says that every insurer has different underwriting guidelines when it comes to life insurance for diabetics.

Even still, Irving says that most insurers care about your age at the diagnosis. “Being diagnosed earlier in life means there’s more time for related complications to develop,” he explains. That may make it harder to get coverage.

Most insurers will also care about any severe diabetic complications. “Having a diabetic coma, an amputation, or a hospitalization are the big three they care about,” says Irving. “But having any one doesn’t mean you can’t get coverage.”

Finally, people with Type 2 diabetes typically have an easier time securing life insurance than people with Type 1 diabetes.

Life insurance for diabetics is often (but not always!) more expensive.

People in good health who don’t smoke generally get better life insurance rates than people with health conditions and smokers. That said, Jake says he’s had diabetics qualify for preferred insurance rates. Preferred is the best rate category available for life insurance.

Nontraditional plans are an option.

One nontraditional option is graded life insurance. With this option, your beneficiaries only receive a percentage of the full life insurance payout if you pass away before a set waiting period. A typical waiting period is two years.

Another option is guaranteed issue life insurance. With this option, you get a limited amount of coverage on the spot. You are not required to have a medical exam or even answer any medical questions. Just know that you may only get a limited amount of coverage and that the rate may be high. There’s also often a waiting period as well.

Controlling your diabetes can help you get better coverage.

Life insurers look more favorably on diabetics who are working on managing their condition. This could mean regularly visiting your doctor, taking your prescribed medication, maintaining a healthy weight, and having lower A1C and glucose levels.

Jake says that it may even be possible to secure a better rate once you control your diabetes. This is especially true if a good amount of time has passed since a hospitalization from diabetes. (Just know that the incident may remain on your health record and affect your rate.)

Working with a licensed insurance agent is your best bet.

Ideally, you want an independent agent who has relationships with many different life insurance companies. This means they can shop around for the best possible coverage for you. It also means they can turn to other carriers if your application is rejected.

You might even consider an agent like Jake who works with high-risk applicants. These kinds of agents are especially knowledgeable about which carriers are most likely to offer you the best policy.

Start the process by learning how to choose a qualified insurance agent. An easy way to find a qualified insurance professional in your area is to use our Agent Locator.

By Amanda Austin

Originally posted on LifeHappens.org

2 replies on “What to Know About Life Insurance for Diabetics”

Thanks for this amazing article…I really appreciate.

Great article! Finding a reliable Life insurance brokerage in Australia is crucial for securing the best deals to protect both life and investment. Thanks for sharing these valuable insights!